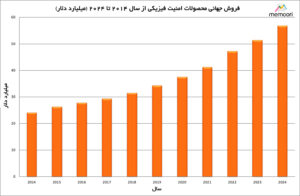

Memory’s 2019 Annual Report on the Physical Security Business shows that the total value of the global physical security products at the factory gate was about $34.31 billion in 2019. This figure represents an 8.5% increase compared to 2018, while the compound annual growth rate over the past 5 years has been only about 7.24%.

Considering that from 2012 to 2017, global gross domestic product (GDP) growth averaged about 2.7%, this growth is significant, and hence the growth of the physical security business has surpassed it by a factor of 2.6%.

Over the past 10 years, this market has grown at a compound annual growth rate of 6.27%. We predict that by 2024, the market will be worth $56.76 billion, growing at a CAGR of 10.72%, although each of the three businesses (access control, video surveillance, burglar alarms) and geographic regions will have significantly different growth rates.

As Western manufacturers compete with their Chinese competitors, video surveillance has had the highest growth rate of 9.74% over the past three years, but their penetration of China’s public sector business is still very low. China is by far the largest market, accounting for perhaps 30-40% of global demand.

Access control systems were also expected to perform better, up 8.2 percent, as they drove more IP network businesses and deepened penetration in biometrics, identity management, wireless locking systems, and access control as a service (ACaaS). This is the third consecutive year that this segment has had the highest growth rate of the three businesses, but pricing issues, partly through consolidation and supply chain weaknesses, are putting pressure on growth. This has slowed growth when measured by value.

The burglar alarm business, the father of the physical security business, has been maturing for a long time, but the growing use of radar and thermal and multi-sensor cameras has driven growth of 3.8 percent in 2019. Additionally, advances in sensor technologies, wireless technologies, and integration with video surveillance, access, and exterior lighting have all contributed to its growth. We acknowledge that there may be a number of video surveillance products installed in PP/IA projects, but these types of products are not considered in this segment count, which could be detrimental to the growth of this segment.

Unbalanced and unhealthy demand structure in the video surveillance business

We have shown in our report that the problem for foreign manufacturers to capture a share of the Chinese market is not a matter of technology or performance, but rather a political and geopolitical challenge.

The reason is that the Communist Party controls even private companies that produce video surveillance systems, and if they want the state-owned business (which today accounts for more than 50 percent of the Chinese video surveillance market) and support with long-term, cheap loans, they must comply with the government’s requirements and demands.

That is why the government ensures that foreign equipment is not used in public sector projects. It is not surprising that such an agreement has eliminated the possibility of “free trade” and allowed the two largest Chinese manufacturers (Hikvision and Dahua) to account for more than 40 percent of the global video camera business. This is partly due to the establishment of a “race to the finish” (a term in economics that refers to a government’s deregulation of the business environment and taxes in order to attract or keep economic activity within its borders. This phenomenon, which is a consequence of globalization and free trade, usually occurs when competition for a particular industry or business activity between governments increases.) to lower prices that no other producer can match because they do not have the same production volume.

The end of this may not be a happy one, though. In this area, there are other Chinese companies that want a piece of this huge investment in the state-owned safe city projects. Huawei, one of the world’s largest telecommunications companies, has announced a major entry into the video camera space, and a new AI video analytics startup called Megvii is aiming to offer comprehensive video surveillance solutions. They will undoubtedly gradually gain ground in the public sector market, taking market share away from the two current Chinese giants, and at the very least, it will ease the pressure on non-Chinese manufacturers operating in more open global markets.

Market Forecast to 2024

Our forecast for the next five years to 2024 is based on the assumption that global trade will not improve and that gross domestic product (GDP) growth will be very low in the next two years. The past 5 years of data show that the physical security business can grow exponentially in a weak economic environment, as new technology is improving product performance and continuously reducing the cost of ownership.

The likelihood of terrorist attacks subsiding in the next 5 years is very low, and government budgets to combat this issue will increase, which will also benefit the physical security business. In the business world, the demand for more comprehensive communication between the three sub-sectors of the physical security business and business units, with the help of Internet of Things (IoT) technology, will grow. This will be evident by 2020, with growth accelerating over the next 4 years.

We predict a 10.7% compound annual growth rate in value over the 5-year period from 2019 to 2024. The main drivers of this growth will be AI video analytics software, which will grow from its current tiny size to $3.5 billion by the end of 2024, creating more demand for video surveillance hardware.

These reports are taken from the 11th edition of Memory’s annual report, “The Business of Physical Security 2019-2024.”

Source: a&s magazine